Executive Summary: The Structural Regime Shift

- The Old World: A 40-year era where the 40% bond allocation reliably offset the 60% equity exposure.

- The New World: A regime of “Fiscal Dominance” defined by 6% deficits, 4% GDP, and potential overheating.

- The Risk: “Implicit Yield Curve Control:” which acts as a hidden tax on traditional bondholders and cash savers.

- The Strategy: Transitioning at the margin from “coupon-clipping” to “real asset” ownership (Gold, Industrial Metals, Commodities) to protect purchasing power.

For forty years, investors benefited from a structural “peace dividend, ” a unique combination of tech-driven efficiency and massive deflation from imported goods. That era is over. The staggering moves in precious commodities and the stickiness of long rates this year is the market’s way of acknowledging that the “40” side of the portfolio, the traditional bond allocation, is no longer a reliable offset to the equity risk on the “60” side.

Historically, these asset moves have served as the precursors to significant inflationary liftoffs and generational regime shifts. We believe that a generational regime change began a year ago, as we highlighted in our Q3-2024 Investment Commentary. Those adhering to backward-looking models run the risk of significant misallocation in their portfolios. Our thoughts from a year ago have not changed much since we wrote:

“As many long-time TwinFocus clients are aware, we believe that gold is a reasonable and logical holding for any investor looking to improve risk-adjusted returns; the current status quo of larger and larger fiscal deficits funded by promissory notes ensures that gold will continue to have value as the antidote to this trend.” October 2024

As the “Run It Hot” investment theme transitions from a fringe macro-thesis to the dominant consensus, US policymakers have hit a wall; they must now prioritize aggressive growth and debt monetization over price stability. They are intentionally running the engine at hot temperatures because, in a world of 6% deficits and 4% GDP, the math of “low and slow” policy no longer works.

The Shift to Fiscal Dominance

We believe we have entered a regime of Fiscal Dominance. Recent actions by global central banks and our own Federal Reserve point clearly to a more dovish positioning. As a testament to the dovishness or the willingness of central banks to cut at the slightest sign of slowdown, there are currently more announced rate cuts globally than during the height of the financial crisis in 2008.

Furthermore, the fiscal push is accelerating. According to Goldman Sachs, the economic impact of fiscal spending is forecast to boost the economy next year by 1.2%. Currently, the deficit is running at 6% of GDP, a level not seen since 2008 or the post-WWII era. This is highly unusual; typically, large government expansions occur during periods of economic slack to minimize inflation. With US GDP at roughly 4%, it is hard to see the justification for the fiscal push, and the markets seem to agree with us.

Karen Ward, Chief Market Strategist for EMEA at JPMorgan Asset Management, recently captured the political reality: “The reason markets have remained so buoyant is because it’s increasingly clear that governments will spend their way out of all political predicaments.”

The Return of the Bond Vigilante

If we look very closely, we can see “bond vigilante” behavior returning to the capital markets. The 10-year forward rates for every country in the G7 are now higher than current 10-year rates, which signals unease with the massive supply of debt coming in the years ahead.

If the bond market begins to continue to act in this manner, the government’s response from reserve currencies is rarely to spend less, rather, it is to control the market. This leads us to the likely endgame, Implicit Yield Curve Control (YCC), or said another way, continuous Quantitative Easing. For the private investor, this is effectively a hidden tax on savers. If the government caps the interest, you earn while inflation runs hot, your real wealth is being redistributed to pay down the national debt. Recent Fed announcements and the push to lower rates, despite 4% GDP, are the beginning of this shift, in our opinion.

We believe that on December 20, post the Fed meeting, we began another round of quantitative easing. Jerome Powell and the committee signaled a willingness to prioritize growth and liquidity over inflation targets; this subtle language change represents a softening of tone over the prior three decades, where generally price stability was paramount to economic growth. These comments feel very out of place to long-time Fed watchers.

The sharp macro team at Strategas highlighted this risk in their recent note:

“How could growth be slowing, but the Fed needs to hike? We don’t know exactly, but the outlook for 2027 may call for exactly that if inflation proves sticky above 3.00%, but the Fed chooses to ease one or more times in 2026.”

The point here is just that it is unusual to cut rates aggressively to raise them shortly after, but that might be the path.

Taking all this together, it’s odd with an economy near full employment to have a central bank focused on growth and to have fiscal spending accelerating. It’s clear to us that policymakers will do whatever it takes to ease the economic soft spots.

The Bitcoin Caveat

Interestingly, Bitcoin (BTC) has not worked as a global money offset, despite fans claiming its magical properties as a libertarian currency. While Bitcoin captures the headlines of speculation, sovereign actors are quietly returning to the foundational assets of the global economy as demonstrated by large gold purchases from central banks globally since the beginning of the Ukraine war where the weaponizing of the SWIFT global banking exchanged encouraged some countries to diversify holdings into gold and away from some dollar-based assets.

To date, BTC has performed as a proxy for QQQ (Nasdaq 100) leverage rather than a proxy for monetary debasement. We are anxiously watching its performance in the coming months, as it is too early to claim it will not eventually benefit from debasement. Historically, however, the correlation currently lies with tech volatility, not monetary and fiscal expansion. Interestingly, BTC has no correlation to the US dollar and a negligible correlation to gold, but a very strong correlation to the QQQs and even higher (65%) to ARKK, Cathie Wood’s speculative high-flyer ETF.

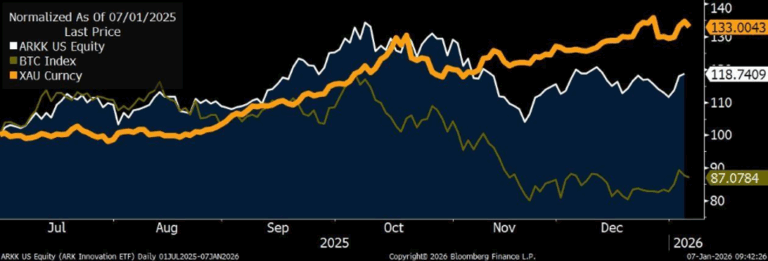

Shown below is the performance of Gold, the QQQ’s and BTC since July 1, when Trump threatened Powell’s handling of the economy directly. While the narrative surrounding Bitcoin suggests it should act as a “digital gold” or a hedge against monetary debasement, the data tells a more nuanced story.

We believe it is important to report the facts: over the past several years, Bitcoin has exhibited a much tighter correlation to high-flying, speculative tech stocks than to traditional debasement hedges.

For example, while gold has trended upward almost uninterruptedly this year, both Bitcoin and Cathie Wood’s flagship fund (ARKK) have struggled. This divergence occurred simultaneously as the market began to question the valuations of some of the highest-flying, low-profitability tech stocks. Shown below is the performance of Gold vs ARKK and BTC, notice the strong performance for Gold since the July 1 and the relatively weak performance of the other assets, especially since mid-September.

Our point is not that Bitcoin lacks value, but rather to highlight that its historical behavior has become that of a “Risk-On” asset, specifically a proxy for tech-driven leverage. While it may eventually mature into a monetary hedge, its current correlation at 65% to speculative growth ETFs suggests it is not yet acting as an offset to the demise of traditional currencies. We believe investors should view it through that lens: as a high-volatility growth play rather than foundational ballast.

Where Should We Invest?

Most wealth models are built on the recency bias of the last three decades, where generally in risk-off environments equities fell, but bonds prices rose in response to lower yields. Our suspicion is that it is less true today, and that stocks and bonds are becoming more correlated in risk off environments as the next crisis comes from an inflationary shock, not from a deflationary one.

While only one data point, during the recent first quarter drop in the market, long duration bonds and stocks fell as the world contemplated an inflationary pulse. In addition, for most of the past 120 years, except for the last 30 years, stocks and bonds have generally moved in unison, meaning they were not hedges, but rather correlated.

To protect capital in a “Run It Hot” regime, we must look beyond central-bank-priced assets and diversify into holdings that are uncorrelated to central bank-set rates. In this environment, being overexposed to long-dated municipal bonds, long-dated treasuries, or long-dated investment bonds is not a true diversifier; rather they may present simply more of the same risk.

We have ranked our strategies from Spicy to Extra Spicy to Holy Moly, in deference to the iconic Porsche Cayenne ads. We specifically focus on the “40” side of the portfolio as we believe it is more at risk of underperformance in a “Run It Hot” scenario.

Spicy

Replace 10% of the bond/credit portfolio with 50% Gold and 50% Global Commodities. This adds ballast with limited risk to relative returns. One should expect this portfolio to offset some of the risk from implicit yield curve control, providing a buffer if inflation remains consistently above our 3% base case. As noted in the purpose-driven note, the 90%/80% should focus on most attractive expected risk-adjusted returns, suggesting little allocation to corporate bonds given tight spreads and preference for uncorrelated idiosyncratic returns (tax liens, asset-backed, special situations) while avoiding publicly traded BDCs. We recommend CLOs but spreads there have also tightened.

Extra Spicy

Replace 20% of the aggregate portfolio currently allocated to bond/credit, with 50% Gold and 50% Global Commodities. This gives investors a fighting chance of generating positive real returns in a bond portfolio. This allows for significantly improved diversification and improves returns as inflation continues to rise.

Holy Moly

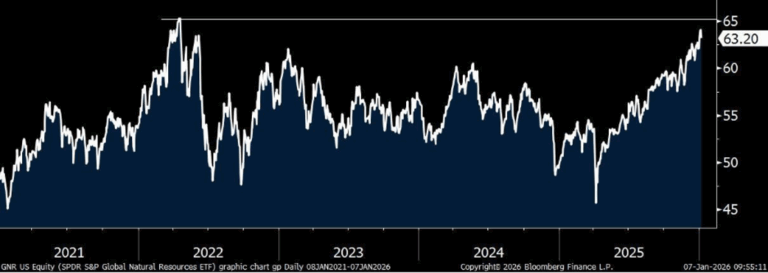

Same 20% replacement as just above, plus replacing 10% of the bond portfolio with equities specifically designed to offset rising inflationary pressures (please reach out to your family office team leader to discuss how to position this trade). Shown below is the 5 year performance of the S&P Global Natural Resource ETF, notice that while performance has been strong of late, it still has not made a new high. We believe the recent performance is a recognition of the “Run it Hot” theme.

We believe that decades of global underinvestment in the commodity complex is finally coming to a head. Key resource areas like Canada, Australia, Peru, Brazil, and Chile are home to the critical resources the world requires, yet the capital to extract them has generally been declining for two decades.

We believe that exposure to these countries will function as an imperfect hedge against global monetary debasement. In this scenario, rising commodity prices act as a powerful catalyst: driving up equity multiples, boosting corporate earnings, and strengthening the local currencies of the most exposed nations.

Interestingly, this entire asset class has been dormant for the last two decades. However, as we write this, it is beginning to break out to new highs. Historically, such a breakout from a multi-decade base is a primary signal that a much larger structural move is just beginning.

Conclusion

The investment approach of the last 40 years has been built for a world of deflation, supported by import deflation and moderate tech deflation. We now live in a world of fiscal dominance and dovish central banks. We believe under that scenario, a “Run It Hot” economy is more likely, and as a result, owning longer duration assets will not function as their traditional hedge to a slowing economy.

Memorandum Disclaimers & Disclosures

This Memorandum is confidential and may contain legally privileged and proprietary information of Twin Focus Capital Partners LLC (“TwinFocus”). It is intended solely for the use of the Recipients to which it is addressed. If you are not the intended recipient, you are hereby notified that any dissemination, copy, disclosure, use or action taken based on this Memorandum or any information herein is strictly prohibited and may be unlawful. If you received this Memorandum in error, please contact the sender immediately and destroy the material in its entirety, whether electronic or hard copy.

This Memorandum may not be otherwise redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without the express written consent of TwinFocus.

Investments involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. In some cases, securities, strategies and other financial instruments may be difficult to value or sell and reliable information about the value or risks related to the security, strategy or financial instrument may be difficult to obtain. Income from such securities, strategies and other financial instruments, if any, may fluctuate and that price or value of such securities, strategies and instruments may rise or fall and, in some cases, investors may lose their entire principal investment. Foreign currency rates of exchange may adversely affect the value, price or income of any security or financial instrument mentioned in this Memorandum. Investors in such securities and instruments effectively assume currency risk.

Hedge fund and other alternative investments are generally unregulated and considered inherently very risky and you can lose material portions of your principal in very short periods of time. Prior to making any investments in any hedge fund managers and alternative investment strategies, you should review all subscription documents and confidential offering memoranda provided by the managers/strategies, paying particular attention to the risk disclosures. You should not invest in such managers/strategies if you are not thoroughly comfortable with these risk disclosures or do not understand and/or appreciate the increased levels of risks associated with such strategies. Additionally, this Memorandum may provide information regarding private funds/strategies/investments which are exempt from registration under the Investment Company Act of 1940 pursuant to Section 3(c)(1) and/or 3(c)(7) which were offered as private placements in reliance on Regulation D of the Securities Act of 1933. Each individual fund/strategy and NOT TwinFocus shall have the sole responsibility for (i) formally qualifying prospective investors to ensure they meet the suitability criteria to invest in each relevant fund/strategy and, once qualified, (ii) sending the formal offering documents and other materials to each prospective investor.

Any information relating to the tax status of financial instruments and/or strategies discussed herein is not intended to provide tax advice or to be used by anyone to provide tax advice. Recipients are urged to seek tax advice based on their particular circumstances from an independent tax professional.

Any waiver by Twin Focus of any section of this Memorandum Disclaimer Statement should not be construed as a general waiver of any other section and/or the entire Memorandum Disclaimer Statement.

The information, including but not limited to forecasts and estimates, in this Memorandum was obtained from various sources and TwinFocus does not guarantee its accuracy. Although the information contained in this Memorandum is from sources believed to be reliable, no representation or warranty, expressed or otherwise, is made to, and no reliance should be placed on its fairness, accuracy, completeness or timeliness.

This Memorandum may contain multi-year financial pro forma planning projections, predictions, return assumptions, as well as other financial, legislative, statutory and client balance sheet assumptions that are for illustrative purposes only and no representations or warranties, expressed or otherwise, are made to, and no reliance should be placed on their fairness, accuracy, completeness, or timeliness.

Past performance is not indicative of future results and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable, equal any corresponding historical performance level(s), be suitable for client portfolios or individual situations, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. As such, all opinions, projections and estimates are as of the date of the Memorandum and are subject to change without notice. TwinFocus is under no obligation to update this Memorandum and Recipients should therefore assume that TwinFocus will not update any fact, circumstance or opinion contained in this Memorandum unless specifically requested. TwinFocus and any director, officer or employee of TwinFocus do not accept any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this Memorandum or its contents.

This Memorandum may contain current opinions of third-party authors and not necessarily those of TwinFocus. Such opinions are subject to change without notice.

This Memorandum may contain references to market indices. Such information is presented to show the general trends in certain markets for the periods indicated and is not intended to imply that the strategy(s) discussed and/or reviewed are similar to the indices either in composition or element of risk. TwinFocus does not make any representations as to whether the indices may or may not be unmanaged, not investable, have any expenses and may or may not reflect reinvestment of dividends and distributions. Index data is provided for comparative purposes only. A variety of factors may cause an index to be an inaccurate benchmark for a particular portfolio/manager/strategy and the index does not necessarily reflect the actual investment strategy of the portfolio/manager/strategy discussed and/or presented in the Memorandum. Current period returns may be estimates. Actual index returns and/or estimates are calculated and presented to Twin Focus through third party software providers and as such, may differ from the final figures produced by the index provider.