The Case for Japanese Equities

Over the past decade, Japan has evolved from a value trap to a more compelling long-term equity opportunity. This shift is being driven by policy initiatives and structural reforms in corporate governance that directly target capital efficiency, liquidity and shareholder value. As a result, the return on capital of Japanese stocks has converged with developed markets while the total shareholder payout ratio has increased. There is room for continued improvements while valuations remain attractive relative to global equity markets.

Notable policy initiatives include the following:

- In 2023, the Tokyo Stock Exchange (TSE) announced plans to accelerate previous reforms, requesting that listed companies implement “management that is conscious of the cost of capital and stock price” through strategies that improve profitability, raise valuation metrics and earn investor confidence. The TSE outlined expectations for policies to improve specific profitability and market valuation targets in a form easy for investors to understand. Noting that a P/B (price-to-book) ratio below 1 indicates company profitability does not exceed its cost of capital or that “investors are not seeing enough growth potential” while even if the P/B ratio is above 1, companies should target further improvement. Companies that did not comply faced delisting or being moved to a lower section of the exchange.

- The Japan Exchange Group (JPX) is revising the TOPIX (October 2026 launch date) to improve liquidity (value of shares trading), broaden coverage and to make it a more investible representation of Japanese equity market. This includes setting new selection criteria that requires companies to increase the number of free-float shares (excluding cross-holdings) to remain in the TOPIX.

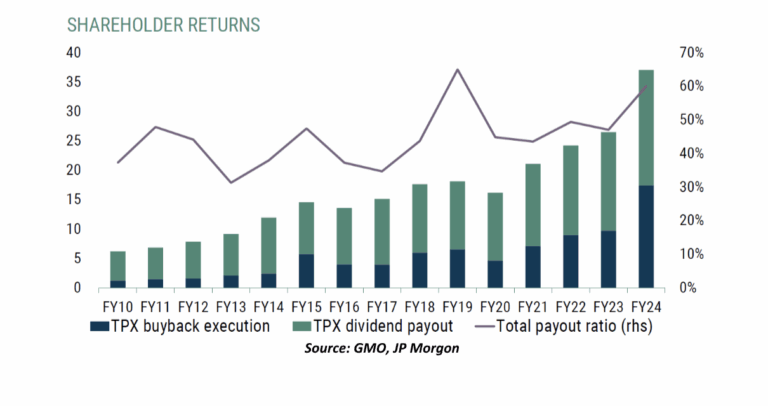

These policy goals incentivize companies to shed non-core holdings (cross-ownership shares and real estate) and cash to repurchase shares or issue dividends. As a result, total shareholder payout ratio has risen with Japanese companies setting an all-time high in buybacks in 2023–2024.

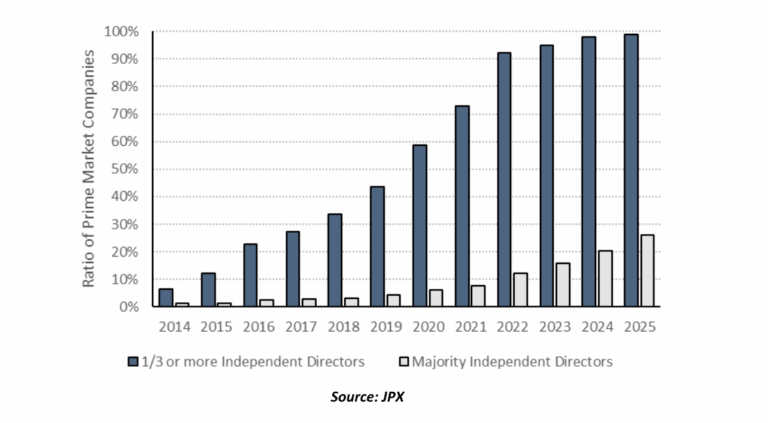

There has also been notable improvement in board/management/shareholder alignment with an increase in stock-based compensation from under 500 companies in 2013 to over 2,500 in 2025 and increasingly independent boards.

This has translated into solid performance for Japanese equities, outperforming the S&P 500 YTD through 10/31/2025 with the lowest P/B ratio SMID-cap stocks the best performing segment since the TSE announcement in March 2023. Importantly, there appears to be room for continued progress and upside for Japanese stocks over the next few years.

- Valuations have risen. Forward P/E ratio is above the 20-year average, but Japanese equities remain relatively attractive compared to US markets.

- The improvement in company fundamentals since the early 1990s, largely encompassing the economic stagnation of the Lost Decades, has been nothing short of historic; on par with economies emerging from deep recessions or developing markets undergoing structural upgrades. Return on equity has more than doubled and is now around 10%. While more competitive, it remains well below other global markets. In addition, asset turnover remains well below developed market peers, suggesting the reform cycle is still in its early stages and that fundamentals have further room to improve.

- The shift from deflation to inflation stands to reshape companies, consumers, and the broader economy. Lazard forecasts Japanese earnings growth to increase from 2% to 13%, on par with the US and EM, in 2026. Households, in response to inflation, are reallocating their assets away from non-interest-bearing assets like currency and deposits toward riskier options like equities.

- Japanese regulators seem focused on the largest stocks trading below a 1x P/B target ratio. The number of stocks trading below a 1x P/B ratio has declined; within the TOPIX from 43% in July 2022 to 28% from). However, within the TOPIX, 580 of 1,670 stocks still trade below a 1x P/B ratio with market capitalizations < $4B.

- The divestiture of non-core assets and return of capital shareholders through buybacks and/or dividends is expected to continue, supported by increasing activism. 2025 has seen a record number of activist proposals and M&A activity as private equity becomes more active.

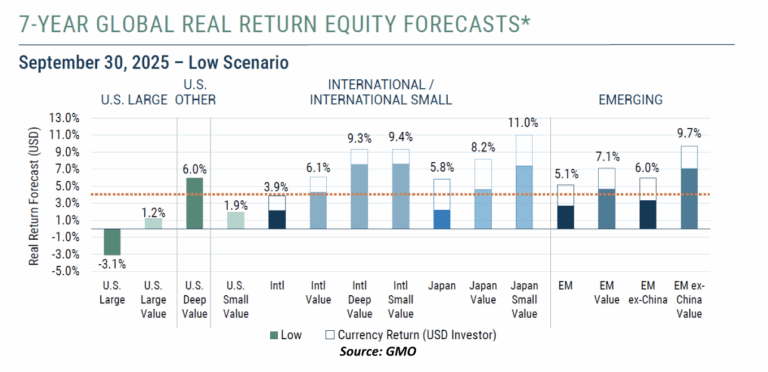

This potential is reflected in GMO’s 7-year real return forecasts, led by USD returns to Japanese small-cap value stocks.

Corporate governance and regulatory reforms are actively unlocking Japanese equity value. For long- term investors, there is a case for a dedicated Japanese equity allocation as part of a fully invested, globally diversified portfolio. There are several ways, varying by strategy, liquidity and cost, to gain exposure to Japanese equities, including:

- A passive ETF providing liquid, lower cost exposure to smaller-cap companies with high dividend-paying or buyback stocks.

- An active mutual fund with a fundamental, long-term, value-oriented approach focused on SMID-cap stocks.

- A hedge fund providing targeted exposure to SMID-cap companies with P/B ratios <1x offering monthly redemptions with 30-day notice and no lock or gate.

Memorandum Disclaimers & Disclosures

This Memorandum is confidential and may contain legally privileged and proprietary information of Twin Focus Capital Partners LLC (“TwinFocus”). It is intended solely for the use of the Recipients to which it is addressed. If you are not the intended recipient, you are hereby notified that any dissemination, copy, disclosure, use or action taken based on this Memorandum or any information herein is strictly prohibited and may be unlawful. If you received this Memorandum in error, please contact the sender immediately and destroy the material in its entirety, whether electronic or hard copy.

This Memorandum may not be otherwise redistributed, retransmitted or disclosed, in whole or in part, or in any form or manner, without the express written consent of TwinFocus.

Investments involve numerous risks, including, among others, market risk, counterparty default risk and liquidity risk. In some cases, securities, strategies and other financial instruments may be difficult to value or sell and reliable information about the value or risks related to the security, strategy or financial instrument may be difficult to obtain. Income from such securities, strategies and other financial instruments, if any, may fluctuate and that price or value of such securities, strategies and instruments may rise or fall and, in some cases, investors may lose their entire principal investment. Foreign currency rates of exchange may adversely affect the value, price or income of any security or financial instrument mentioned in this Memorandum. Investors in such securities and instruments effectively assume currency risk.

Hedge fund and other alternative investments are generally unregulated and considered inherently very risky and you can lose material portions of your principal in very short periods of time. Prior to making any investments in any hedge fund managers and alternative investment strategies, you should review all subscription documents and confidential offering memoranda provided by the managers/strategies, paying particular attention to the risk disclosures. You should not invest in such managers/strategies if you are not thoroughly comfortable with these risk disclosures or do not understand and/or appreciate the increased levels of risks associated with such strategies. Additionally, this Memorandum may provide information regarding private funds/strategies/investments which are exempt from registration under the Investment Company Act of 1940 pursuant to Section 3(c)(1) and/or 3(c)(7) which were offered as private placements in reliance on Regulation D of the Securities Act of 1933. Each individual fund/strategy and NOT TwinFocus shall have the sole responsibility for (i) formally qualifying prospective investors to ensure they meet the suitability criteria to invest in each relevant fund/strategy and, once qualified, (ii) sending the formal offering documents and other materials to each prospective investor.

Any information relating to the tax status of financial instruments and/or strategies discussed herein is not intended to provide tax advice or to be used by anyone to provide tax advice. Recipients are urged to seek tax advice based on their particular circumstances from an independent tax professional.

Any waiver by Twin Focus of any section of this Memorandum Disclaimer Statement should not be construed as a general waiver of any other section and/or the entire Memorandum Disclaimer Statement.

The information, including but not limited to forecasts and estimates, in this Memorandum was obtained from various sources and TwinFocus does not guarantee its accuracy. Although the information contained in this Memorandum is from sources believed to be reliable, no representation or warranty, expressed or otherwise, is made to, and no reliance should be placed on its fairness, accuracy, completeness or timeliness.

This Memorandum may contain multi-year financial pro forma planning projections, predictions, return assumptions, as well as other financial, legislative, statutory and client balance sheet assumptions that are for illustrative purposes only and no representations or warranties, expressed or otherwise, are made to, and no reliance should be placed on their fairness, accuracy, completeness, or timeliness.

Past performance is not indicative of future results and there can be no assurance that the future performance of any specific investment, investment strategy, or product will be profitable, equal any corresponding historical performance level(s), be suitable for client portfolios or individual situations, or prove successful. Due to various factors, including changing market conditions and/or applicable laws, the content may no longer be reflective of current opinions or positions. As such, all opinions, projections and estimates are as of the date of the Memorandum and are subject to change without notice. TwinFocus is under no obligation to update this Memorandum and Recipients should therefore assume that TwinFocus will not update any fact, circumstance or opinion contained in this Memorandum unless specifically requested. TwinFocus and any director, officer or employee of TwinFocus do not accept any liability whatsoever for any direct, indirect or consequential damages or losses arising from any use of this Memorandum or its contents.

This Memorandum may contain current opinions of third-party authors and not necessarily those of TwinFocus. Such opinions are subject to change without notice.

This Memorandum may contain references to market indices. Such information is presented to show the general trends in certain markets for the periods indicated and is not intended to imply that the strategy(s) discussed and/or reviewed are similar to the indices either in composition or element of risk. TwinFocus does not make any representations as to whether the indices may or may not be unmanaged, not investable, have any expenses and may or may not reflect reinvestment of dividends and distributions. Index data is provided for comparative purposes only. A variety of factors may cause an index to be an inaccurate benchmark for a particular portfolio/manager/strategy and the index does not necessarily reflect the actual investment strategy of the portfolio/manager/strategy discussed and/or presented in the Memorandum. Current period returns may be estimates. Actual index returns and/or estimates are calculated and presented to Twin Focus through third party software providers and as such, may differ from the final figures produced by the index provider.